Invest Or Pay Off Student Debt

The #1 question that I hear from new optometrists or current students that are on the cusp of graduating is:

“Should I begin saving for retirement right now or should I delay saving for retirement and focus on paying down my student loans as quickly as possible?”

With the majority of new ODs graduating with a student loan balance the size of a decent home mortgage, debt management and balancing that responsibility along with life’s other responsibilities weighs heavily on new OD’s.

I’ll highlight a few key considerations and thoughts to consider when making the decision to invest or pay off student debt for yourself and your family.

Your income is your greatest wealth building tool and being as efficient and effective with the finite dollars that you bring home on a monthly basis is what will allow you to build a solid financial foundation now and for the future.

The idea of lumping student loans into a debt snowball is a subjective decision in and of itself.

What I mean by this is the lost opportunity in compounding interest that occurs if you decide to put off saving for retirement and pay down all of your debt.

It’s my intention to show you “both sides of the coin” and then insert the X-factor of human emotion and behavior into the equation in the last segment of this trilogy.

Feeling overwhelmed by student debt? 💰 Check out our handy Student Loan Repayment Calculator! 🙌

Setting the Stage

For this and the two articles that will follow, let’s assume that we have a new grad optometrist that recently graduated with $200,000 in a 30-year, federal consolidated student loan at 6.8% and is making $100,000 as a W-2 employee of a practice.

From here, we’ll evaluate three scenarios to help investigate the question - invest or pay off student debt:

- aggressively paying off debt

- aggressively saving for retirement (and staying in debt for the duration of the loan)

- a hybrid approach

Aggressively Pay Down Debt

In order to pay down your debt as quickly as possible, we need to first look at how much “ammunition” we’ll have to accomplish that task. Let’s look at our sample OD’s annual income:

Add on “life’s basic necessities” of health, auto, renters/homeowners, life, and disability insurance, rent/mortgage, food, possible car payment, gas, cell phone, and other basics and you can quickly see how $5,779 per month can get eaten up pretty quick and the ammo that’s left to chip away at your student loan mountain is minimal.

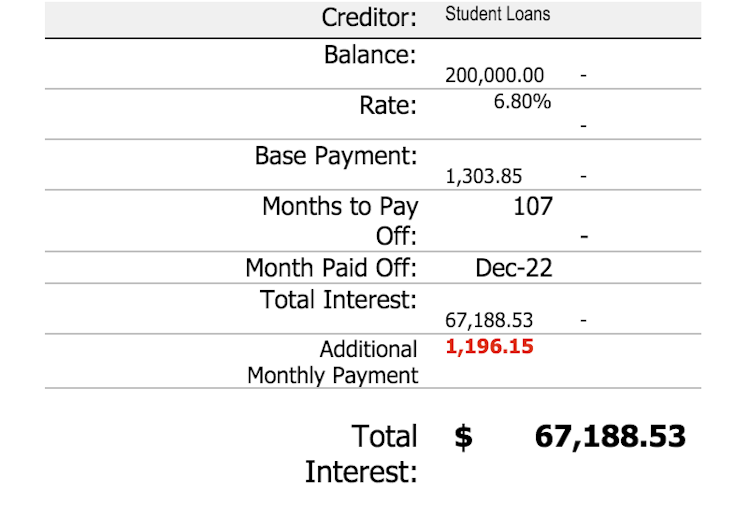

Assume you get “lean and mean” and are able to put $2,500 per month to pay towards your student loans. The loan calculation looks as follows:

This means that in 107 months, or just under 9 years, you’d be debt free from your student loans.

Keep in mind that we haven’t thrown kids, a mortgage, a spouse, any type of “wants,” travel, professional development courses, etc. into this equation.

If that monthly payment drops down to $2,000 per month (an additional $696/mo), we’re now pushing 12+ years before being debt free.

‘Feeling inspired yet? ‘Thought so…

The Opportunity Cost

“Opportunity cost” is defined as what one has to give up in order to have something else.

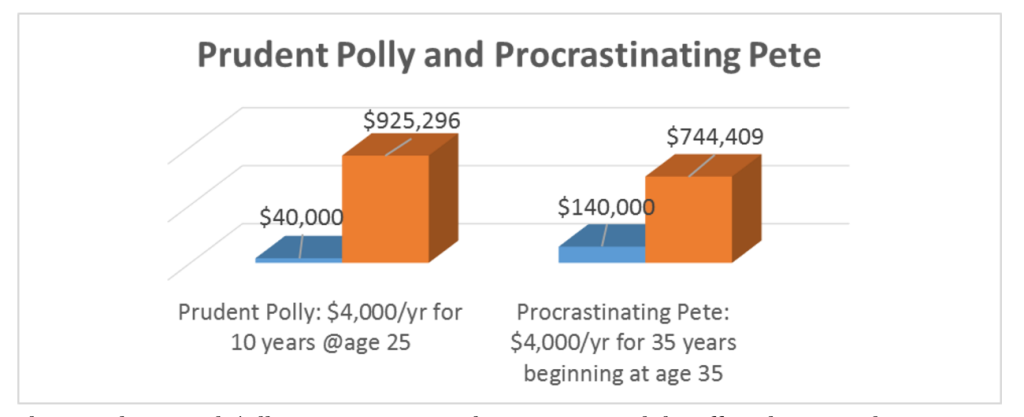

In this case, it’s best to illustrate the scenario of Prudent Polly and Procrastinating Pete and how compounding interest works when it comes to investing.

In the “Tale of Two Investors,” Prudent Polly invests $4,000 a year at age 25 for just ten years…and then stops.

At an assumed 8% annual rate of return, her total investment of just $40,000 would grow to $925,296 before taxes by the time Polly is 70.

On the other hand, Procrastinating Pete doesn’t start investing until ten years later at age 35, and then he invests $4,000 every year for the next 35 years, through age 70.

The results are amazing.

Pete stashes away $140,000, or $100,000 more than Polly, but he is not able to make up for lost time.

Although Polly invested much less money, the total value of her investment at age 70 exceeds Pete’s by over $180,000 before taxes.

This simple example* illustrates compounding interest and the effect that it can have on someone’s nest egg, especially if they forego investing for the estimated 9 years or 12+ years that we illustrated above.

The Icing on the Cake

As I advise all OD’s that we work with, life only gets more expensive with every birthday that we have. Whether it’s kids and their infinite number of activities, a house, a practice/business, aging parents, a boat or camper, or a number of other “things,” life somehow has a way of becoming more expensive.

This illustrates even more the importance of having a plan, sticking to the plan, and re-evaluating your progress on a periodic basis. As is said in business and is true in financial planning, “What gets measured, gets done.”

In the second chapter of our trilogy we’ll look at the impact of starting to save from an early age…and the opportunity cost of keeping loans around for a much longer period of time.

*These examples are hypothetical and for illustrative purposes only. The rates of return do not represent any actual investment and cannot be guaranteed. Any investment involves potential loss of principle.