Avoid Lifestyle Creep & Establish a Solid Financial Foundation Early in Your Career

I get it. You’ve busted your tail to get to this point of your life. You’ve endured undergrad plus 4 years of optometry school. Some of you have even possibly done a residency. During all of this time you’ve been forced to live pretty much any combination of frozen dinners and boxed meals and have moved more times in those eight years than you ever care to move for the rest of your life! You’re ready to settle down and set up shop (literally from a professional sense or proverbially in your personal life). You’ve sowed a lot of great seeds…time to reap!!

Here is a 27 page ebook dedicated to understanding finances for optometrists and paying off student loans.

Hold on, though. Let’s pump the breaks.

Before you throw caution to the wind and think that you’ll be able to “make it rain” now as an OD (yes, I actually had a client come in and use that phrase), let’s run some numbers and get a true understanding of what you can afford and what you need to be aware of early on in your profession so that you’re not setting yourself up for failure in the long run.

On the surface, it may seem like you have all the money in the world. After all, for most new ODs, your first month’s earnings are more than you were probably asked to live off of for an entire semester!

Don’t let those money habits disappear, though!!

You were frugal then because you had to be frugal. You still need to be frugal, or rather responsible. The difference is that the implications of a wrong decision now may not come home to roost for years, possibly decades.

Without a plan, purpose, and intention the shiny objects, advertising, and emotional urge to make unplanned and expensive decisions can have a significant impact on your long-term plans.

There are four decisions (and action items) that I feel can significantly hamper your long-term financial health. Not being cognizant of these decisions can cause both long term implications and short term misuse of funds.

Lack of student loan awareness.

Most student loans enter a six month grace period following graduation, which means that your first student loan payment doesn’t come due until December after graduation (Happy Holidays). You don’t HAVE to let this 6 month period go without paying them back. Remember, if your loans are unsubsidized, interest begins accruing from the day you took out the loan, so every day that passes, you are earning more and more interest and will thus have to pay back a higher balance.

Action item: call all of your lenders and understand what the total monthly payment will be on your student loans and understand the various payment options (PAYE, REPAY, PSLF, etc.)

Start Saving for Financial Independence (Retirement) NOW!

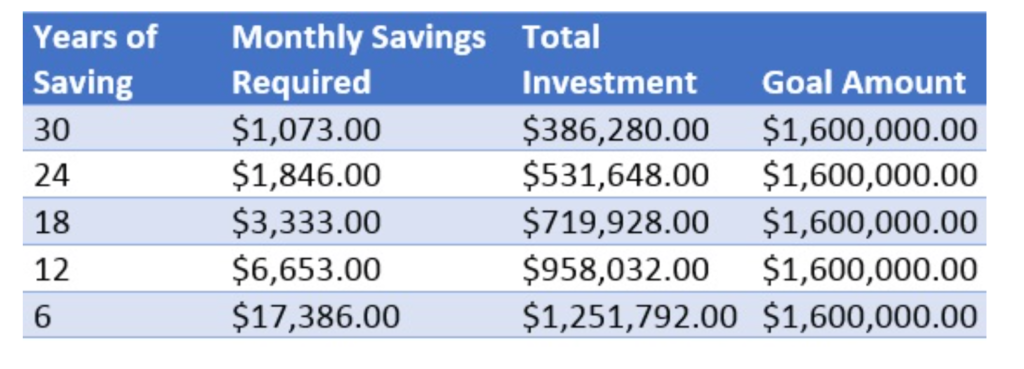

Time and money are two finite resources in life, but they have an interesting correlation and relationship: with more time, you can make more money. With more money, though, you cannot make more time. Pause and take a moment to re-read that statement, because it’s a very profound thought.

If we assume a goal of trying to save to $1.6 million, the chart below illustrates the variables included, articulates this philosophy of time, and also shows the power of compounding interest.

A general rule that I have is that unless you can pay off all of your loans in 5 years or less, you should not delay saving for retirement. You’ll never be able to “catch up” and life never gets less expensive as you get older.

Action item: begin saving for retirement in a retirement account such as a Traditional or Roth IRA, 401(k), SEP, SIMPLE IRA, etc. Conduct your own due diligence or work with a qualified financial professional to help you evaluate which type of account and how much to begin saving.

You Don’t Need a New Car.

You may not even need a newer car. If it has four wheels, isn’t being held together with chicken wire, and gets you from Point A to Point B, guess what: it’s serving the purpose of what a vehicle was designed to do for you! So many Americans spend so much money on cars they don’t need to impress people they don’t know and will never see again.

Understanding finances for optometrists is a topic not frequently discussed. In this Episode of The Vision, we cover personal cash flow statements and how to use our Google Sheets tool!

With the average new car payment at $515 and used car payment at $371 per month, it’s easy to see how vehicles can get in the way of wealth building and be a damper on one’s ability to grow their wealth. Vehicles are a depreciating asset…we’ve all heard the fable of how much a car’s value drops as soon as “you drive it off the lot.”

I get the question of buy vs. lease a lot, and we’ll discuss that in a future article.

In the meantime, here are some basic ideas and rules to live by when it comes to vehicle purchases:

- NEVER buy new unless you can afford to pay cash

- Buy used, preferably CPO (certified pre-owned)

- Put as much down as possible (again, ideally pay cash)

- Understand GAP insurance coverage and whether you need it.

Don’t become house rich, cash poor.

Contrary to what your parents may say, you don’t NEED to buy a house right away and it’s not always “the responsible thing to do” or “what adults do.” You don’t need to immediately “start building equity” in a house and you’re not just “throwing money away by renting.” As you can see, I’ve heard it all from my clients (and their parents) on some common myths on home ownership.

There are many reasons why home ownership may not be right for you at this point in your life. You may not be sure where you want to settle down. You may not have enough saved for a healthy down payment. If you’re starting your practice cold, most mortgage underwriters will require 2 years’ business tax returns to consider you for a mortgage.

In order to “break even” on buying a house, you should plan on staying in your house for at least 6 years. Selling any sooner typically means that you will be at a loss (compared to just renting) during that time. This is because of a variety of factors, including estimates for home repairs and maintenance (landscaping, minor home improvement projects, etc.), realtor fees (when you sell), as well as interest payments on your mortgage (you pay the most interest as a percentage of your monthly mortgage payment in the beginning of your mortgage).

Continuously buying and selling homes during short timespans is a sure-fire way to hamstring your ability to become financially independent, especially if they are done using the 30 year mortgage.

Conclusion

Getting a handle on these four principles can ensure that you don’t let the “bright and shiny objects” of today get in the way of building a solid financial foundation that will bring you closer to financial independence in the future.

*The chart presented in this article assumes an 8 percent return and the reinvestment of all earnings. Return figures are for illustrative purposes only and do not represent the past or future performance of any actual investment, nor should they be used as investment advice. Example assumes investment is made at the end of each month and the reinvestment of all earnings, but does not take in account any applicable fees, expenses or any taxes.