We had probably received no less than a half dozen different direct mail pieces from financial companies talking about “refinancing student loans” and what that could mean for my wife, Andrea.

As a relatively recent Class of 2011 graduate from the

IU School of Optometry, Andrea (like a large number of her fellow colleagues) were burdened and battling a mountain of student loan debt.

As most recent graduates find out, even when you crunch the math in school and learn what your estimated loan payment is going to be, it doesn’t quite hit home until your loans come out of deferment and that first payment is due in December.

From my vantage point, it’s a story I see play out all too often.

I offer a very unique viewpoint on all of this, because in addition to being married to an optometrist, I’m also a CERTIFIED FINANCIAL PLANNER

TM Practitioner and the founder of

Integrated Planning & Wealth Management, LLC and specialize in serving practicing optometrists, their families, and their practices.

We take a comprehensive planning approach in our work with OD’s, and while succession and retirement planning is the focus of our seasoned OD’s, the recent classes of OD’s are fighting a different battle: finding the delicate balance between debt management, monitoring cash flow, and living the quality of life they aspire to live after putting in nearly a decade of effort into their professional education post-high school while not coming at the sacrifice of financial security and independence in the future.

My wife and I are not unlike most of you reading this article.

Unless you were fortunate enough to have had means provided to you to pay for not only your undergraduate education but also 4 additional years of optometry school, the amount of student loan debt that you’re saddled with is weighing on your mind on a weekly (possibly daily) basis and it influences almost every decision that you make with your money…and therefore your life.

The best way one can not have that burden anymore is to pay off their debt.

However, looking at a student loan balance that would put anyone in a decent sized home in most Midwestern suburbs would seem to be no short order.

The Process Begins:

Let’s go back to the beginning where I talked about those direct mail pieces.

Being a numbers guy and always trying to maximize the return on our income and build towards financial independence for our family, I was always looking for ways to be more efficient and effective with our dollars.

Each time I’d see the direct mail piece come in the mail, I’d open it up, glance at it, and think what I’m sure a lot of other people have thought of when looking at the information that was presented: “Gotta be too good to be true. What’s the catch?”

Been there, done that.

Multiple times over.

However, at this point I knew that Andrea and I didn’t want to be nearing retirement and first then celebrating being debt free from her student loans, so I decided to start “peeling back the layers of the onion” and doing some due diligence on one of the companies that had sent us a number of mailings.

I read press releases. I read newspaper articles.

I tore through their disclosure and disclaimer documents (the link is at the bottom of most websites). I read reviews and talked to other CFP® Professionals that had student loan experience and expertise, and then I started the refinance process on behalf of my wife to get a first-person perspective on what I hoped would be a great resource for not only our family but so many others.

The Numbers and Data:

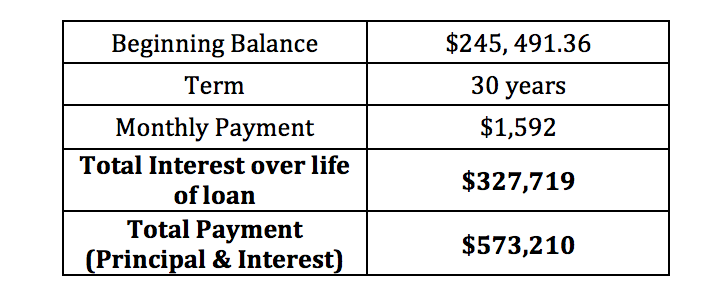

Let me first share with you her current student loan details as they were structured through

EdFinancial from her original consolidation:

When you plug that into any loan calculator, you will find the following facts that are associated with these loan values:

It still makes us sick to our stomach to look at when we think of how much we could have potentially paid to her student loans over 30 years (had we taken that long to pay them off).

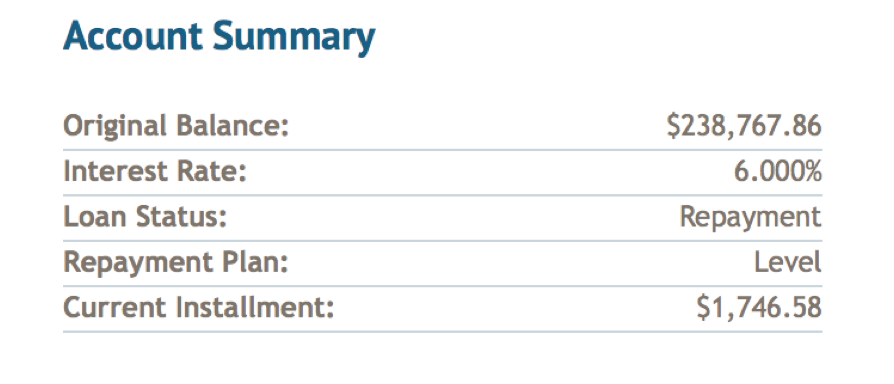

Upon receiving the official offer letter from the underwriter with our new terms and rate for her loans, I immediately started crunching the numbers to see what that meant for us going forward under her new 20 year loan.

Here are the details:

In addition the lower interest rate we’d received, we’re also receiving a rate discount because we’ve signed up for automatic payment on a monthly basis.

Double win: one less thing to worry about and we save even more in interest.

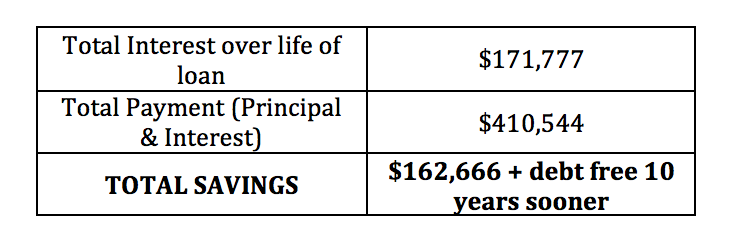

When we put those dollars into the same loan calculator, we come up with the following:

As you can see, you don’t need to be a personal finance guru to know that $162k+ is a lot of coin to be saving over the duration of your loan, not to mention that we’re able to be debt free 10 years sooner.

The Fine Print

While we were able to be debt free 10 years sooner on this straight payment schedule, it’s also important to know that a lot of these institutions can work and accommodate a number of different repayment schedules…even doing 30 year loans.

However, a general rule is that the longer the duration of the loan, the higher the interest rate and the more you’ll pay in overall cost of the loan. This is where it’s important to crunch all of the numbers on your situation. Additional point: make sure your lender does NOT penalize you for early prepayment, so once you get to a point financially where you can afford to pay extra on your loans and pay them off even earlier (as we plan to do), you can certainly do that without prepayment penalties or repercussions.

You’ll notice that our payment did go up a bit on a monthly basis; however, when you break that down on a daily basis, that’s about $3.90 per day.

To save that much I’ll forgo that daily Starbucks® and make my coffee at home or choose to pack my lunch a couple of more times per week rather than going out to eat.

Simple exchanges like that for the benefit of what I just illustrated is just one of the many ways that you can win financially.

Please keep in mind that while there are a lot of similarities between these financial institutions refinancing loans and the federal government student loan program, there are two concessions that everyone should be aware of:

- you give up the traditional “income-based repayment program” that is offered

- you will no longer be able to qualify for the Federal Student Loan Forgiveness program

In the end, everyone’s situation is different and I will always encourage you to perform your own due diligence along with other advisor(s) that have your best interest at heart when looking at these types of solutions to determine which strategy will serve you and your family best.

Here’s to your continued success and continuing to advance the profession of optometry and provide quality eye care to all the patients you serve.

Registered Representative, Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC. Investment Advisor Representative, Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. IP&WM & Cambridge are not affiliated.

Refinancing your student loans? Check out this free comparison tool from our partners at Credible:

Disclosures: Adam Cmejla, CFP® nor Integrated Planning & Wealth Management (IP&WM) are not affiliated or related in any way to any financial institution offering student loan refinancing options nor should this be interpreted as an endorsement for any specific institution. Readers should perform their own analysis on their situation and understand the full financial implications of their decisions. The article and content should not be interpreted as personal financial advice and should not be used as the sole piece of information in a decision making process. Adam nor IP&WM do not provide student loan refinance solutions for optometrists. This information is being provided for informational purposes only. The opinions and information presented is that of the author and does not in represent those of any other publication that chooses to share or reprint this article.